Life Insurance for Beginners: Everything You Need to Know

A comprehensive guide to understanding life insurance basics.

Are you starting to think about protecting your loved ones' financial future? Life insurance can be a critical part of that process.

From understanding the different types of policies to knowing how much coverage you need, navigating the world of life insurance can feel overwhelming. Let’s break it down.

This guide is designed to provide clarity, helping you make informed decisions about your family's security.

Life insurance is a contract. You and an insurance company make this contract. You pay premiums. The insurer gives a lump-sum payment, a death benefit, to your beneficiaries when you die. Why is it important? It gives your family or dependents financial security after you are gone. This ensures they can pay for daily living, a mortgage, education, and other debts.

This beginner's guide covers everything you need to know about life insurance. It covers the different types of policies and how to decide the right coverage for your needs. This article will give you the knowledge to make smart decisions about protecting your loved ones.

Quick navigation

What is Life Insurance?

Life insurance is a financial product. It gives your loved ones a financial safety net if you die. It is a contract between you (the policyholder) and an insurance company (the insurer). You pay regular premiums. The insurance company pays a lump sum of money, the death benefit, to your beneficiaries when you die.

The main purpose of life insurance is to replace income lost when you die. It helps your beneficiaries pay essential expenses. These include mortgage payments, childcare, education costs, and everyday living expenses. It helps your family maintain their standard of living and financial stability even after you are gone. It is a step to ensure your family is taken care of, no matter what happens.

How does it work?

Types of Life Insurance Policies

There are several types of life insurance policies. Each has its own features, benefits, and costs. Understanding these different types is key to choosing the right one for you. Let's look at the main types:

Term Life Insurance: Term life insurance covers a specific period, or “term.” If you die during this term, your beneficiaries get the death benefit. If you live longer than the term, the policy expires. There is no payout. It is usually the most affordable type of life insurance because it is simple.

Whole Life Insurance: Whole life insurance is a type of permanent life insurance. It covers you for your entire life, as long as you pay premiums. It also has a cash value component. This grows over time on a tax-deferred basis. You can borrow against this cash value or use it to pay premiums.

Universal Life Insurance: Universal life insurance is another type of permanent life insurance. It offers more flexibility than whole life. It combines a death benefit with a savings component. It also lets you change your premium payments and death benefit within certain limits.

Variable Life Insurance: Variable life insurance is a type of permanent life insurance. It lets you invest the cash value portion of your policy. You can choose from investments like stocks and bonds. The death benefit and cash value can change based on how these investments perform.

Do you know which one is right for you?

How Life Insurance Works

Getting life insurance involves several steps. First, you apply for a policy. You give personal information, including your age, health, lifestyle, and financial details. The insurance company then assesses your risk. They often do a medical exam. They use this to decide your premium. If approved, you pay premiums. You can pay monthly, quarterly, semi-annually, or annually.

When you die, your beneficiaries need to file a death claim with the insurance company. They will need to provide a death certificate and the policy number. The insurance company will review the claim. If approved, they will pay the death benefit to your beneficiaries. The speed and ease of this depend on the insurance company and the completeness of the documents.

It is important to name your beneficiaries. You must keep that information up to date, especially after major life events. These include births, marriages, and divorces.

Key Life Insurance Terms

Understanding the common terms used in life insurance can help you understand the policies. It also helps you make informed decisions. Here are some key terms:

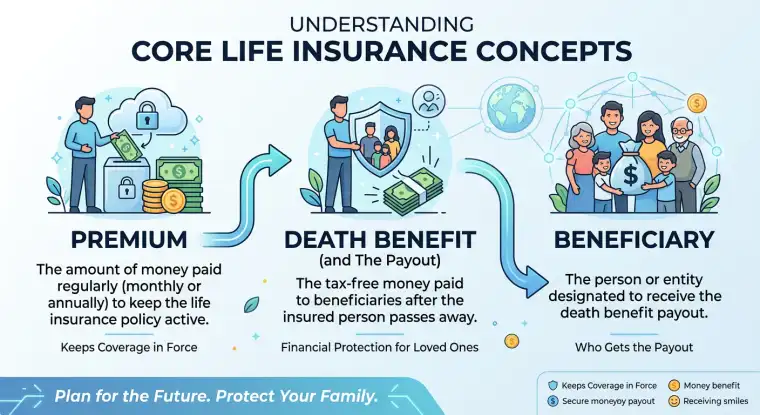

Beneficiary: The person or entity that gets the death benefit from your life insurance policy.

Premium: The regular payment you make to the insurance company to keep your policy active.

Death Benefit: The money paid to your beneficiaries when you die.

Policy: The legal contract between you and the insurance company. It outlines the terms of your coverage.

Cash Value: The savings component of a permanent life insurance policy. It grows over time on a tax-deferred basis.

Coverage Amount: The total money the insurance company pays when you die.

Underwriting: The process an insurance company uses to assess your risk. They use this to decide your premium.

Wouldn't it be easier if there were a simple guide for all of this?

Factors Affecting Life Insurance Costs

The cost of life insurance is affected by several factors. Insurance companies use these to assess risk. These factors help determine the premium you will pay. Understanding these factors can help you anticipate the cost. It can also help you find the best rates.

Age: Generally, the older you are when you apply, the higher your premiums will be. The risk of death increases with age.

Health: Your health is a key factor. Those in good health usually pay lower premiums. Pre-existing medical conditions, like heart disease or diabetes, can increase premiums.

Lifestyle: Risky habits, such as smoking or drinking too much alcohol, can lead to higher premiums. Insurance companies assess risk based on lifestyle choices.

Coverage Amount: The higher the death benefit, the higher the premium. The amount of coverage you choose affects the cost.

Type of Policy: Term life insurance is usually less expensive than permanent life insurance policies. This is because of the shorter coverage period and no cash value component.

Gender: Women tend to live longer than men. Women often get lower premiums.

Considering all these factors, is life insurance actually attainable?

What this means for you

Life insurance is important for financial planning. It is especially important for those with dependents. It gives you peace of mind. You know your loved ones will be taken care of financially after you are gone. Choosing the right policy, understanding the terms, and considering your situation will give you the coverage you need to protect your family's future.

Life insurance helps you provide for your family, even when you are gone. It helps with covering debts and paying for final expenses.

How do you get started?

Risks, trade-offs, and blind spots

Life insurance offers benefits. It is important to know the potential risks, trade-offs, and blind spots. Not considering these things can lead to less-than-optimal financial planning. Premiums can be expensive. They increase with age and health conditions. This cost can sometimes strain a budget, making it hard to afford the coverage.

Term life insurance only provides coverage for a specific period. If you live longer than the term, you may need to renew the policy at a higher rate. You might need to find a new policy. It is also important to read the fine print. Some policies may have exclusions or limitations. They may not cover death by suicide within the first two years of the policy.

Not having enough coverage is a major blind spot. Many people underestimate the amount of life insurance they need. This leads to not enough financial protection for their beneficiaries. This can cause financial hardship for your loved ones.

Main points

Life insurance is important for financial planning. It provides security for your loved ones. Here is a summary of the key takeaways:

- Types of Policies: There are different types of life insurance. These include term, whole, universal, and variable life insurance.

- Coverage Needs: Assess your financial obligations to decide how much coverage you need.

- Premiums: Premiums are affected by age, health, lifestyle, and the type of policy.

- Beneficiary: Name beneficiaries and keep the information updated.

- Cash Value: Permanent life insurance policies often have a cash value component.

- Exclusions: Know about potential exclusions or limitations in your policy.

- Professional Advice: Talk to a financial advisor to decide the best plan for you.

- Ongoing Review: Review your policy regularly to ensure it meets your current needs.

Understanding life insurance basics is the first step to securing your family's financial future. Take time to evaluate your needs, compare your options, and make an informed decision. By doing this, you will be one step closer to providing peace of mind. You will know your loved ones are protected.